Introduction

The US-Israeli war on Iran has not only been a military confrontation with geostrategic dimensions. It has also revealed just how deep the connections are between geopolitical security and global economic stability. The war has had complex strategic and economic repercussions, particularly as regards the Strait of Hormuz. The Strait is no longer simply a vital shipping route for some of the most important global strategic commodities, first and foremost oil and gas. It is now also a means of exercising pressure, a tool for geopolitical attrition capable of inflicting serious damage on the global economy – in particular for those countries that have particularly strong commercial ties with the Gulf, and for the countries of the Gulf themselves.

The wide-ranging threats and restrictions that have affected shipping through the Strait, and the attendant supply chain disruptions, have produced an unprecedented state of anxiety in global energy markets. This has had repercussions, to varying degrees, for all the world’s markets – in particular those of Asian countries, which are highly dependent on Gulf oil and gas imports. This is no longer just a matter of price fluctuations or high prices, not to downplay the inflationary consequences these have for consumers and producers and the pressure on public finances. There are now real threats to security of supply, threats that pose a real and direct danger to the stability of economic activity and of daily life.

Historical precedent, countries’ differing strategic visions, and the differing capabilities, possibilities, and policies that these visions produce all mean that there is variation in how states approach challenges and crises. Some states seek to contain the consequences of these crises and make it easier to accommodate to them by adopting austerity policies, providing temporary subsidies, or passing some of the cost on to producers and consumers (or some combination of the above). But these approaches, notwithstanding the responsiveness and short-term flexibility that it affords, remain essentially reactive, rather than proactive or pre-emptive. Often, they mean simply swimming with the current of crises, and prevent economies from developing long-term structural resilience.

Other states, meanwhile – in particular China – are inclined to take advantage of crises and challenges in order to reassess their economic models and make them more robust. This is particularly true in the case of problems that have now become endemic to the global economy, given rising geopolitical tensions and increasing interconnectivity of supply chains and markets.

I: A Global Quest to End Fossil Fuel Dependency

Growing awareness of climatic and environmental threats, and the emergence of an international consensus around the need to adopt proactive policy in order to confront them, have provided a great boost to the renewable energy sector and to the resources available for research and development of green technology. While human beings have made primitive and simplistic use of mechanical and thermal energy since ancient times, in the modern era renewable energy has undergone unprecedented growth and development. This development, in its earliest stages, was driven by geopolitical concerns: the global crises of the second half of the 20th century, although less complex and protracted than those of today, nonetheless revealed the dangers of excessive reliance on traditional energy sources. These concerns were then bolstered by more deep-rooted environmental and sustainability concerns. The 1973 oil export ban, shortly after the Yom Kippur (October) War of the same year, marked a turning point for the global energy sector. There was worldwide interest in increasing the efficiency of energy consumption and a turn towards developing and adopting alternative energy sources as a strategic choice to strengthen energy security and reduce reliance on fossil fuels.[1]

The real transformation in environmental motivations, however, has taken place since the beginning of the 21st century, with growing concern around the consequences of climate change as various studies have shown that modern lifestyles and a growing reliance on fossil fuels are the main reason for accelerating global warming. This awareness has led to the adoption of far-ranging investment policies to develop clean energy sources, particularly in the developed nations, alongside corresponding policies to limit the consumption of energy from traditional sources. As a result, by 2023, renewable energy had come to account for 30% of global energy production. In 2025, 40% of all electricity produced worldwide came from green sources – in Europe, 47%. Despite the rapid growth of solar power, hydroelectric power continues to account for the largest share of the renewable energy mix.[2]

II: From Environmentalism to Economic Self-Interest

Historically, environmental motivations related to the use of fossil fuels to generate energy have been the main driver of the development of the renewable energy sector. However, the great boom in renewable energy technology, and its proven ability to preserve the environment and reduce levels of harmful emissions, have helped bring about a major shift in motivations for expanding research and development in the field. Originally, the motivation was environmental and moral: it was about protection the future of the earth and the rights of generations yet to come. Increasingly, however, economic and commercial considerations are taking centre stage: a desire to reduce energy costs for the productive and service sectors and for consumers. This shift has become particularly important in recent years amid a dramatic expansion of energy-intensive activities, not least with the development of artificial intelligence.

Today, around 80% of the world’s inhabitants still rely on imported fossil fuels, making them vulnerable to ever more frequent geopolitical shocks. This is despite the fact that most countries are blessed with abundant sources of renewable energy – many of which remain untapped. While fossil fuels still account for around 60% of global electricity production, renewable energy is growing much faster. Between 2015 and 2024, renewable energy production capacity grew by around 2,600 gigawatts (140%), while fossil fuel production capacity grew by only around 640 gigawatts, reflecting the rapid turn to alternative energies.[3]

Recent years have seen great improvement in renewable energy production technology and a marked fall in the associated costs, meaning economic concerns have played a more central role in the shift to green energy. Between 2023 and 2024, installation costs for most renewable energy technologies fell by more than 10%, with the exception of offshore wind, which remained relatively stable, and biofuel, whose costs increased. Meanwhile, factors such as funding costs and performance led to a slight increase in the cost of generating electricity using some technologies, such as solar panels, wind farms, and biofuels, while these costs fell sharply for concentrated solar power, geothermal energy and hydroelectricity. As a result, renewable energy continued to consolidate its position as a more price-competitive option: 91% of new capacity was cheaper than the cheapest fossil fuel alternative. Over the course of 2024, renewable energy saved around USD 467 billion in fossil fuel costs, strengthening its role in supporting energy security, economic flexibility and long-term sustainability.[4]

III: Geopolitical Motivations

Despite the great acceleration in the development of renewable energy technologies and their price competitiveness vis-à-vis fossil fuels, there are still technical considerations that prevent us from relying on them totally. This is particularly true of solar power, which can only be produced during the hours of daylight and ceases to function entirely at night – as well as being seasonal, which means that the long winters and short winter days that many countries experience make it less reliable. Nonetheless, technological developments over the coming years and decades, particularly in the field of energy storage, are expected to help us overcome many of these challenges. The International Energy Agency estimates that by 2050, renewable energy sources may account for around 90% of global electricity production, with 70% coming from wind power and solar power and the remainder from nuclear.[5]

Moreover, the current tense geopolitical climate in many parts of the world, which is only likely to worsen over the coming years, as well as growing environmental worries, may accelerate the shift to renewable energy. Asian countries, particularly China, have made a habit of learning from the challenges they have faced. They may choose not to stand idle in the face of threats to their oil and gas supplies, particularly given the strategic importance that this has taken on in light of the shutdowns and restrictions on shipping through the Strait of Hormuz.

The US-Israeli war on Iran may help consolidate a new reality in terms of the consequences that wars and military conflicts can have. We are now in a situation where conflict spilling over into energy infrastructure is no longer a hypothetical scenario but a real possibility. The ability to target energy installations is no longer a card left unplayed – it is now a direct tool for management of conflict which warring parties can resort to in order to make strategic gains. Israel and the US have targeted a number of Iranian energy generation installations, including sensitive infrastructure such as nuclear power plants. Iran, meanwhile, has expanded its retaliatory attacks to include vital energy infrastructure in countries that are not even a party to the conflict, such as Kuwait. This is all taking place within a broader escalatory context, intensified by the use of explicitly threatening political language, such as Trump’s threat to plunge Iran into darkness and destroy its vital infrastructure, including bridges, in the event that his proposed settlement conditions were not met.

These new geopolitical dynamics may help to consolidate a shift in the global power generation model. Major power generation sites, particularly those connected to central grids, are exposed to direct geopolitical and military threats that may accelerate the pace of transformation towards renewable energy sources – but this will take place as part of more decentralized models of implementation and design. These new developments may push countries with a particular strategic vision for their security to increase their reliance on distributed models of power generation, particularly at the level of smaller facilities or even among consumers. This will help reduce reliance on large and centralized power generation infrastructure that can be easily targeted.

IV: A More Strategically Secure and Reliable Renewable Energy

At a time when geopolitical developments are driving a turn towards safer and more reliable forms of renewable energy, there are still technical and capital challenges of great importance that must be confronted. The most important of these is the need for massive expansion of energy storage capacity. Increasing the reliability of renewable energy sources that are inherently unpredictable, in particular solar and wind energy, requires huge investment in storage technology – whether batteries or other innovative solutions – to ensure that they can provide consistent electricity to the domestic, industrial, and service sectors.

Energy storage technology has not been unaffected by the recent wave of development and innovation. Many states and specialist companies have been paying increasing attention to these technologies. The last few years have seen accelerating and marked developments in this field, both in terms of efficiency and of technological diversity, making renewable energy systems more reliable and stable. The world has made great strides in this respect, whether in terms of long-term energy storage, alternative battery chemistry, or improved systems design. As a result, the role of energy storage is no longer confined to short-term load balancing. It now also contributes to better reliability of supply, capacity provision, and ensuring energy security. These are areas that will help make battery storage a fundamental and independent component of the infrastructure of modern electricity systems.[6]

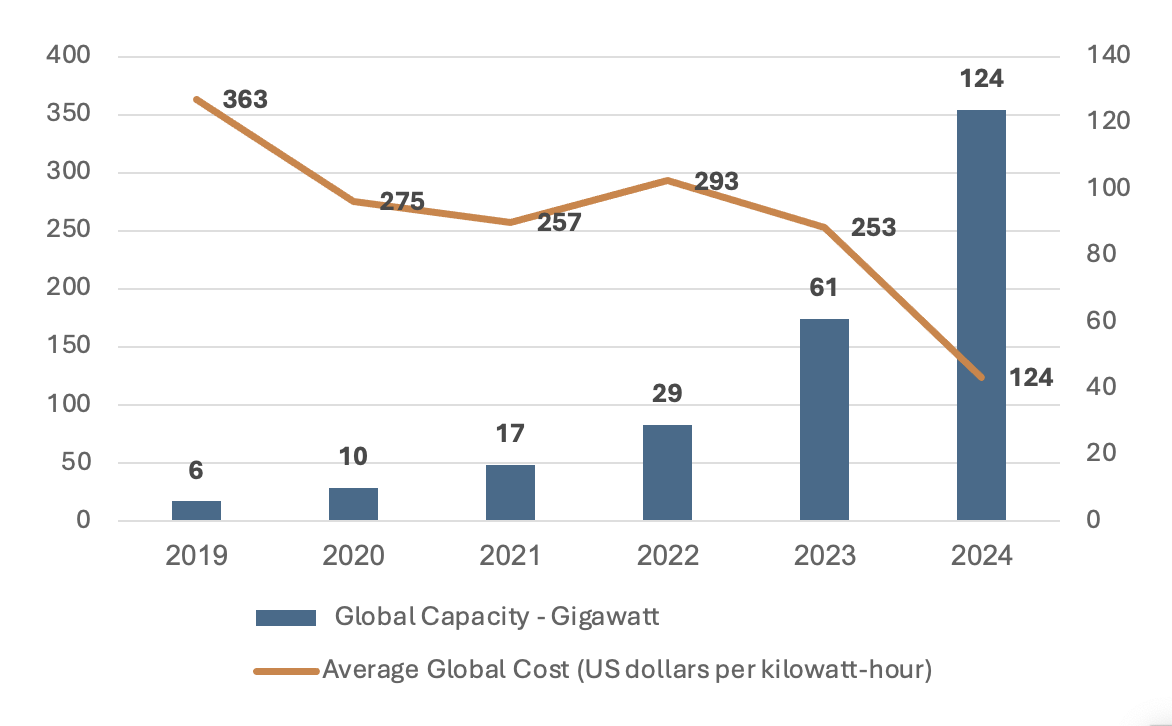

This growing interest in electricity storage systems, alongside rapid improvements in manufacturing techniques and in quality, has had noticeable consequences for the growth of storage capacity worldwide, which has made unprecedented leaps forward over the last decade. Between 2019 and 2024, utility-scale storage capacity increased more than 20 times over, from six gigawatts to 124 gigawatts. This huge expansion coincided with a noticeable decrease in the average cost of batteries, from $363/kwh in 2019 to around $358/kwh in 2024, a fall of around 59%.

Utility-scale battery project costs, VRE share and utility-scale battery storage capacity relative to peak load 2019-2024

Source: “Electricity: Flexibility,” International Energy Agency (2026), accessed on 28/4/2026, at:

https://acr.ps/hBxMvMe

What is noteworthy here is that China, one of the countries that has been most affected by the restrictions on shipping in the Strait of Hormuz, has been a global pioneer in battery production technology, whether with respect to production capacity or to production and sale costs. It continued to lead world efforts to reduce battery costs in 2025, with the average price falling by 13% to around $84/kwh. This fall was driven by a range of factors, most notably the fall of input costs, excess production capacity, the intensity of price competition, and the move towards lower-cost lithium iron phosphate (LFP) batteries. Prices in North America and Europe, meanwhile, remained 44% and 56% higher respectively. Chinese prices for stationary batteries, used to service utilities, also fell to record lows: cell and pack prices fell to around $36/kwh and $50/kwh respectively.[7]

V: Technology as a Baseline; Geopolitical Pressures as a Driver

The Strait of Hormuz’s new role as a key weapon in the US-Israeli war on Iran has forced countries everywhere to come to terms with new geopolitical concerns. These concerns are likely to remain relevant for years, if not decades, to come. They are also likely to have an effect on the security of world energy supplies. For those countries that are keen to learn lessons from the challenges that they face, this new outlook may result in a reconsideration of approaches to energy, energy sources, and energy technologies.

The events of this war – destruction of energy generation infrastructure and threats to completely annihilate it if the conflict escalates – require a reassessment of the design of energy systems worldwide. This is particularly true of those systems that rely for supply on traditional sources concentrated in particular geographical areas, as is the case in most Asian countries, which meet their oil and gas needs through imports from the Gulf. At a time when the direction of travel seems to be towards reduced dependence on traditional sources of energy in favour of an unavoidable shift towards renewable energy, it may be that the model of expansion and the designs of these systems themselves need a rethink. Grid-based systems remain vulnerable to emerging security threats: in the military conflicts of today, they are easy to target and disable, meaning that they cannot be an integrated strategic option. Utility-based systems, meanwhile, are relatively more secure – although if we are to rely on them, we will need to make further advances in reducing the costs and increasing the use of storage technologies (batteries).

In this context, China emerges as the most likely contender to drive this transformation, given the major progress it has already made in battery technology when compared to other countries, not least the US and Europe. It is also the country most vulnerable to a breakdown of oil and gas supplies under current geopolitical conditions, and has a great deal of experience in turning challenges into strategic opportunities.

[1] “From Oil Crisis to Energy Revolution: How Nations Once Before Planned to Kick the Oil Habit,” Rapid Transition Alliance, 16/4/2019, accessed on 27/4/2026m at:

https://acr.ps/hBxMwAM

[2] Anna Francesca Macesar, “The History of Renewable Energy,” The Sustainable Agency, 8/8/2025, accessed on 26/4/2026m at:

https://acr.ps/hBxMvKj

[3] “Renewable Energy: Powering a Safer and Prosperous Future,” United Nations, accessed on 27/4/2026, at:

https://acr.ps/hBxMvXU

[4] Renewable Power Generation Costs in 2024 (Abu Dhabi: International Renewable Energy Agency, 2025), accessed on 27/4/2026, at:

https://acr.ps/hBxMwbv

[5] 5 Net Zero by 2050: A Roadmap for the Global Energy Sector (Paris: International Energy Agency, 2021), accessed on 27/6/2026, at:

https://acr.ps/hBxMwp6

[6] Peter Lawrence & Julia Dinkel, “The Age of Battery Storage - Part II: Structural Demand Drivers and Innovation are Making Battery Storage a Core Grid Asset,” Novogradac, 31/3/2026, accessed on 28/4/2026, at:

https://acr.ps/hBxMwCH

[7] Colin McKerracher, “New Record Lows for Battery Prices,” Bloomberg NEF, 19/12/2025, accessed on 28/4/2026, at:

https://acr.ps/hBxMvZP